Business

Streamlining the road to net-zero through carbon reporting

By Paul Rekhi, Head of Carbon Services at Advantage Utilities

Understanding the evolution of our carbon footprint is key to comprehending the urgency and significance of emission reduction today. According to the Global Carbon Project, between 2011 and 2020, carbon dioxide emissions averaged at 38.8 billion tons per year, but our land and ocean sinks which convert this CO2 have only been able to support 21.7 billion tons yearly. This deficit in emissions is what has caused the atmospheric CO2 growth rate which in turn has led to global warming and climate change. These are defining issues for businesses, hence the need to report and then reduce carbon emissions is more important than ever. I recently hosted a webinar where I discussed this very point, advising businesses on how to implement a credible plan to achieve net-zero as well as lower energy costs.

In this article, I will share those insights, discussing how ESG emerged as a key consideration for businesses today. I will then outline how businesses can go about measuring their carbon by using the carbon-ethics cycle which includes the steps they should take to streamline the road to net-zero via effective carbon reporting.

The distinction between net-zero and carbon neutral

There is an important distinction to be made about what we mean by ‘net-zero’ and ‘carbon neutral’. Net-zero involves counting emissions, then organically removing these emissions from the business. What carbon neutrality involves is the same accounting principle of greenhouse gas (GHG) accounting but also taking accredited carbon offsets to help counteract GHGs released and reaching a zero-carbon footprint. However, to get to true net-zero you have to account for it – that means having oversight into your scope 1, 2 and 3 emissions.

Scope 1 emissions are direct emissions such as company facilities and vehicles. Scope 2 emissions primarily involve indirect emissions stemming from purchased electricity, heating and cooling. Finally, Scope 3 emissions involve everything else your business does; this starts with upstream activities, everything that happens before your organisation – ‘from cradle to gate’, including bought goods, employee commuting and leased assets, through to downstream activities, everything that happens after – from gate to grave, such as processing of solid products, transportation and investments.

The importance of carbon reporting

As corporate guidance emerged and the damaging effects of excess carbon emissions were accepted, this led to large companies being required to report on their scope 1 and 2 emissions. If an organisation meets two or more of the following criteria; a turnover or gross income of £36 million or more; balance sheet assets of £18 million or more; or 250 employees or more; then they must stay compliant with UK government regulations such as theStreamlined Energy and Carbon Reporting (SECR) and Energy Savings Opportunity Scheme (ESOS). Of the 5.5 million UK businesses, only 7,000 fall into the category of having over 250 employees.

But this is not just a checkbox exercise, it is a strategic move. Proper carbon reporting not only ensures compliance but also positions your organisation as a responsible and forward-thinking entity, which is why it has become widely accepted for organisations to establish an ESG department.

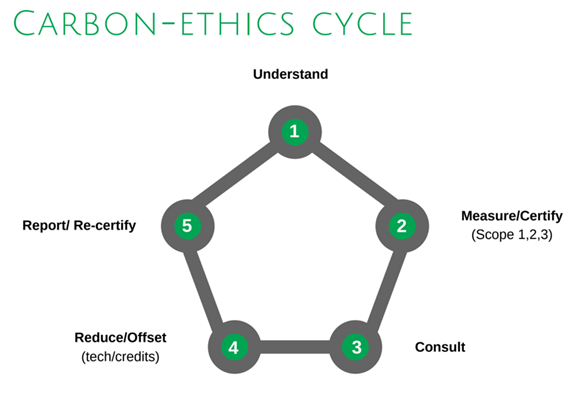

The carbon-ethics cycle

To enable businesses to track their carbon emissions, we created our carbon-ethics cycle, to enable organisations to measure, manage and reduce their emissions as efficiently as possible.

Our starting point is to understand businesses – their sites, their objectives and their needs. From here, businesses should measure and certify their scope 1, 2 and 3 emissions which act as an organisation’s benchmark on how much carbon was associated with their business, within a given period – usually by financial year. Without first measuring emissions, you cannot manage emissions, making progress towards net-zero very difficult.

Once we have that benchmark, consultation with each department of the business is crucial to effectively reducing emissions, looking at how energy is used (when and where) as well as how it is procured. From there, technology such as solar PV, heat pumps and voltage optimisation, can be used to make energy savings and increase sustainability.

Reducing/offsetting emissions may also be necessary if reducing emissions is not possible. The final step is to report and re-certify their emissions, allowing comparisons to be made to benchmark data. And this is an ongoing process, so the cycle can begin again on the journey to net-zero. But what this cycle achieves is a streamlined process that enables the most progress to take place.

So where are we right now? With large companies required to report on their carbon, other companies are also taking it upon themselves to expand their own reporting. There are several types of clients that get in touch with us to measure their carbon and reduce their emissions. One of them are the large companies, but others include organisations with supply chain partners requesting carbon data, companies with competitors measuring carbon emissions, environmentally conscious companies as well as others.

A structure to measuring carbon within your organisation

Businesses all start from the same position: having to change their processes and behaviour in order to measure carbon. Progress is only made by building upon this foundation, with Standard Operating Procedures (SOPs) offering the next step in ensuring compliance throughout the business. On top of that, policies are overlaid which runs and controls the business.

But there are also two ‘floors’ that are missing in this structure. The first of these is accounting, reporting and marketing. Without measuring and accounting what it is that you are doing as a business, the effects of your progress will be minimal, which is why marketing is also crucial to enhancing brand image and customer loyalty. The final step is planning and execution, fundamental to realising your organisation’s goals. This cannot be forgotten as this is where businesses must ensure they have all the experience, expertise, knowledge and skills in place to report for what they do.

To conclude, businesses implementing carbon reporting will find that progress towards net-zero is far easier. The need to reduce emissions is clear and the systematic measurement, management, and subsequent reduction of emissions is made a tangible possibility through the streamlined and efficient approach outlined in the carbon-ethics cycle. A collaborative and structured carbon reporting process allows businesses to meet reduction targets successfully, ultimately leading to the attainment of net-zero status.

PSD3 and the Real-Time Fraud Imperative: What the Regulation Actually Demands of Financial Infrastructure

Why law firms can no longer afford fragmented networks

The compliance cost trap and why efficiency must be the next frontier

How 5G and AI are shaping the future of eHealth

Combating Cyber Fraud in the Aviation Industry